DCRS

|

Navigation: Debt Counselling Guide > DCRS |

·Purpose of DCRS is to allow Consumers to benefit from DCRS concessions to reduce repayment period and to ensure that the Consumers become financially rehabilitated in the shortest possible period.

·DCRS launched in Feb 2011.

·DCRS = Debt Restructuring Rules System.

·DCRS is a central calculator which will verify DCRS calculations.

·DCRS ensures fair and consistent application of concessions.

·The software is centrally located and hosted by independent Hosting Company (Internet Solution).

·Access by DC to verify DCRS repayment rules is only possible via Debt Counselling Systems.

·Access by CPs to verify DCRS repayment rules is only possible via DCRS view only facility via controlled log in.

·Amendments to DCRS rules only possible with full industry consent.

·End goal being that only accredited rules deployed on the DCRS for validation.

Click on the following headings to expand:

|

The method of determining the start date of the DCRS proposal has been changed: ·It will no longer be strictly from the date of validation. ·It will, upon validation, be a combination of next future date on the proposed payment plan and the client's Action Day. ·This date cannot exceed 46 days after the validation date. Below is an example of how the proposal start date is acquired: o Validation date (when the proposal is changed from "Create" to "Provisional") = 2019-09-05. o Next future-dated proposed payment plan date = 2019-09-30. o Client action day = 28. o DCRS proposal start date = 2019-09-28. Daily interest (using the contractual interest rate) will be applied to the obligations from the COB date until after the interim period (the date of first payment to the CP), This will also adversely affect the solve rate of DCRS proposals. |

DCRS process fixes due for incorporation

DCRS process fixes due for incorporation

|

The following DCRS fixes have been approved by CIF:

oLocking of COB information in Debt Review process (implemented).

oFirst Payment date (implemented).

oVAF calculation to be extended to 84 months from inception (implemented).

oSame Reference Number to be used throughout.

oPro-rata interest to be added (from COB to date of first payment).

oNo change to Summary repayment plan.

oThe Z File (preparation file).

oCredit life to be changed to credit insurance. |

|

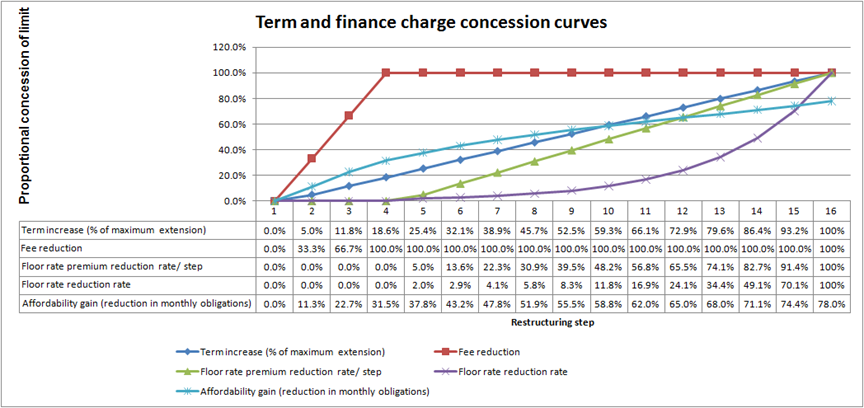

Credit Agreement Rule: Mortgages: Up to 240 months from date of restructure to maximum of 360 months from inception of the loan VAF: Up to 1.5 times contractual term subject to maximum of 90 months from inception and 100 months for accounts with ballooning Deemed contractual term*: Balance up to R1 500: Deemed contractual term 12 months and restructured over 18 months from date of restructure Deemed contractual term*: Balance R1501 to R3 600: Deemed contractual term 12 months and restructured over 36 months from date of restructure Deemed contractual term*: Balance above R3 600: Deemed contractual term 24 months and restructured over 60 months from date of restructure Unsecured: Balance up to R1 500: 18 months from date of restructure Unsecured: Balance R1 501 to R3 600: 36 months from date of restructure Unsecured: Balance above R3 600: 60 months from date of restructure

*In credit facilities, such as overdraft, credit card or store cards, no repayment period is set. In DCRS a deemed repayment period is set in line with extension rules. |

|

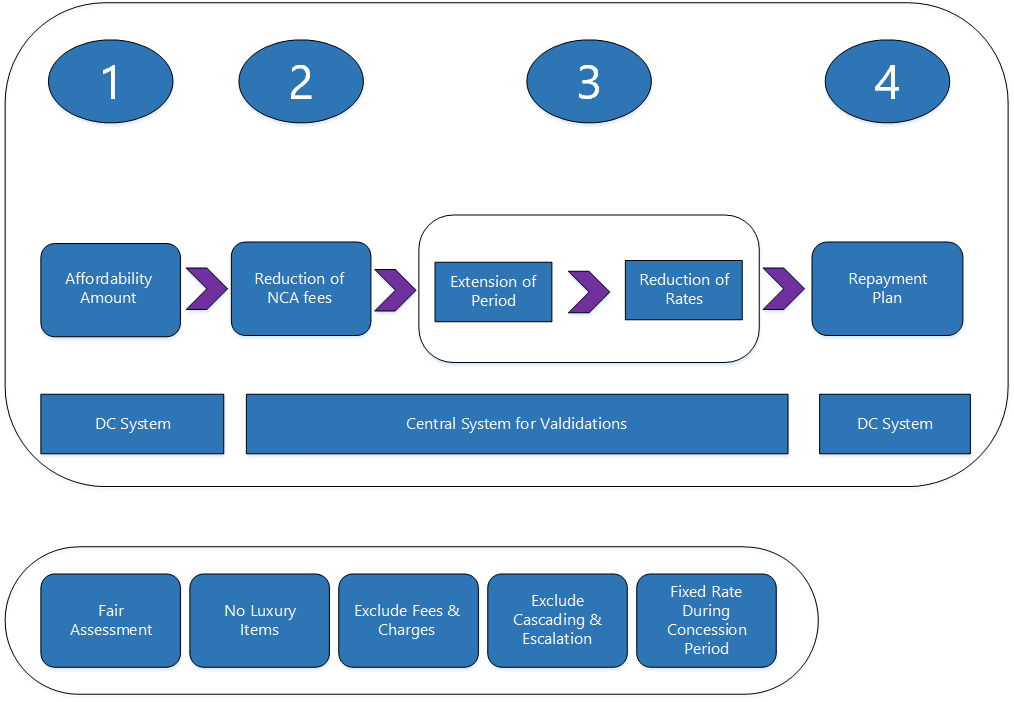

oThe assessment of the Consumer must be reasonable.

oSome Consumers are not eligible.

oUnnecessary assets must be sold to reduce debt.

oMinimum amount must be available to repay debt.

oMinimum amount must be allocated for expenses.

oNo luxury items.

oModerate non-essential expenses.

oAssets must be insured. |

|

Debt Restructuring Highlights

|

|

Before Cascading: Repayment amount R 39

After Cascading: Repayment amount R 39

Reasons why cascading is not used in DCRS oWhen cascading is applied you undertake to increase payment exactly as per the cascaded plan.

oIn cascading repayment is assumed based on COB or information supplied by the Consumer.

oIn practice repayment will NEVER be in line with cascaded plan. Reasons include interest after COB, information supplied by Consumer not accurate, payment timing differences, additional fees, etc.

oIf payment cannot increase exactly as per cascade the CP may commence with legal enforcement.

oThis means if cascading is applied in DCRS the Consumer is set up for failure.

oThe PDA plan should include cascading which should reduce the repayment period.

oReleased affordability is used to repay remaining debt and this will reduce

|

Why should Debt Counsellors use DCRS?

|

oDebt Counsellors will spend less time to restructure proposals.

oNo counter proposal which speeds up the process.

oRestructure rules pre-agreed.

oDebt Counsellors find it easy to sell the benefits of reduced fees and interest rate to Consumers.

oDCRS speeds up the Court process.

oConsumers cash flow benefit can be up to 39%.

oThe Consumers will rehabilitate sooner.

oConsumer benefits from added protection in terms of the NCR Task Team Agreement.

oAdherence to agreed process reduces disputes between the DC and CP. |

|

oThe aim is to repay unsecured debt within 60 months. In practice this may mean 61 or 62 months.

oWhen unsecured debt has been repaid the Bond concessions ends.

oVehicle debt is normally restructured over 84 months from inception of the debt and this may mean repayment that exceeds 60 months.

oThe effect is that contractual fees and interest rate will be applied on the Bond.

oNew repayments should be calculated based on capital outstanding at that point in time, the restructured term and contractual interest rate.

oDebt Counsellors are advised to confirm future repayments when concessions ends with respective CPs and advice Consumers accordingly.

oRepayment plans prior to Clearance Certificate to be amended accordingly.

oDebt Counsellors are advised to inform Consumers of expected payments after Clearance Certificate to avoid legal action. |